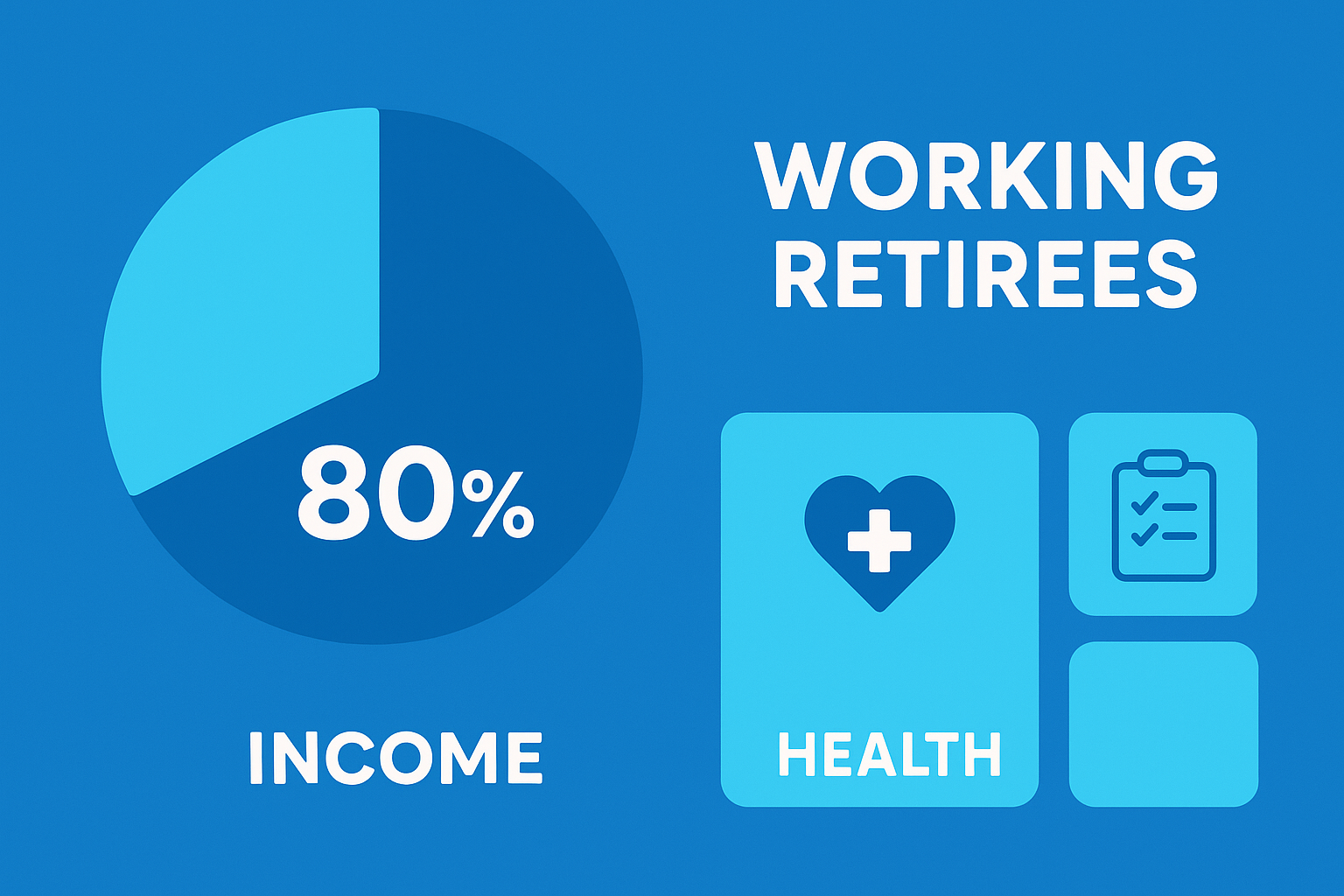

Imagine retiring at 65, only to find your savings need a boost from part-time work to cover rising costs. For most Americans, this isn’t a dream—it’s the plan for 80% of Americans expecting to work post-retirement.

At Davenport & Associates, we help people approaching retirement blend earning and saving strategies.

Why are people working in retirement in 2026? Economic pressures, longer lifespans, and inflation (2.8%) drive this trend, with 25% staying full-time past 60.

This article explores reasons, benefits, and planning tips. How can you plan for working in retirement? Learn how to optimize income and protect assets.

What drives working in retirement? Inflation erodes savings—$50K today needs $68K in 10 years—and Social Security covers just 40% of pre-retirement income.

Longer lifespans mean 20–30-year retirements, prompting 80% to seek supplemental earnings.

Many choose flexible roles like consulting or gig work to maintain purpose and health benefits. Our clients use IRAs and trusts to shield earnings from taxes.

What are the advantages? Financially, it adds $20K–$50K annually, bridging gaps for 70% underprepared retirees.

Emotionally, it combats isolation—working retirees report 20% higher life satisfaction. Health benefits include delayed Social Security claims for higher benefits (up 8% per year delayed).

How does it impact taxes? Earnings can fill Roth IRA contributions, growing tax-free.

What are the downsides? Burnout affects 30% of working retirees, and coordinating benefits with Medicare is complex.

How to plan? Set boundaries with part-time roles and use MoneyGuidePro to model income scenarios. Trusts protect earnings from creditors, ensuring security.

Working in Retirement: Pros and Cons

| Aspect | Pros | Cons |

|---|---|---|

| Financial | Extra $20K–$50K/year, delayed SS | Tax complexity on earnings |

| Emotional/Health | Purpose, 20% higher satisfaction | Burnout risk (30% affected) |

| Planning | Flexible gigs, IRA optimization | Medicare coordination challenges |

| Asset Protection | Trusts shield income | Potential overwork without boundaries |

How to minimize taxes while working? Contribute to Roth IRAs (up to $7,500 in 2026) with earnings, and use trusts for asset protection. Delay Social Security to age 70 for maximum benefits. Our holistic plans integrate work income with retirement savings.

Does working affect Social Security? Yes, earnings above $22,320 (2026) reduce benefits until full retirement age.

Is gig work a good option? Absolutely—platforms like Uber offer flexibility without employer ties. With 30+ years of expertise, we tailor plans for all scenarios.

Working in retirement offers financial security and purpose for 80% of Americans in 2026. Don’t leave it to chance—70% lack integrated plans. Ready to blend earning and saving? Contact Davenport & Associates for a free consultation to optimize your strategy. Schedule now.

John F. Davenport holds a law degree from Pace University, an MBA in finance from Fordham University and undergraduate degree from the University of Notre Dame.

He is a licensed attorney in New York and Connecticut, and a financial advisor.

He founded Davenport & Associates in 1997 and has spent more than 30 years helping CT and NY locally and families across the country build retirement income plans and estate strategies that work together, not against each other.

Davenport & Associates is located at 800 Connecticut Avenue, Suite E401, Norwalk, CT 06854.

Phone: (203) 853-6300 | jdavenportassociates.com

IMPORTANT DISCLAIMER:

Educational only—not investment/tax/legal advice. No strategy guarantees results—vary by rates, markets, laws, personal circumstances. Consult advisors.