Imagine retiring with a $500,000 home, only to face rising costs that threaten your savings. For couples over 50 with $250K+ in assets, your home is a powerful tool to secure retirement. Yet, 70% of Americans lack a plan to leverage it, risking financial strain.

At Davenport & Associates, we help you unlock home equity safely.

What is home equity in retirement planning? It’s the value of your home (minus debts) used to fund retirement through options like reverse mortgages or downsizing.

With 2025’s rising housing costs, this trend is critical. How can you use home equity in 2025? This article explores strategies to boost income and protect assets.

Home equity is your home’s market value minus any mortgage balance. For example, a $600,000 home with a $200,000 loan has $400,000 in equity.

Why is home equity key for retirement? It’s often your largest asset, and with 2.8% inflation in 2025, tapping it can supplement income or protect against Medicaid recovery.

Surveys show 60% of retirees plan to use home equity for income, yet many hesitate due to complexity fears. Our team simplifies this with tailored plans.

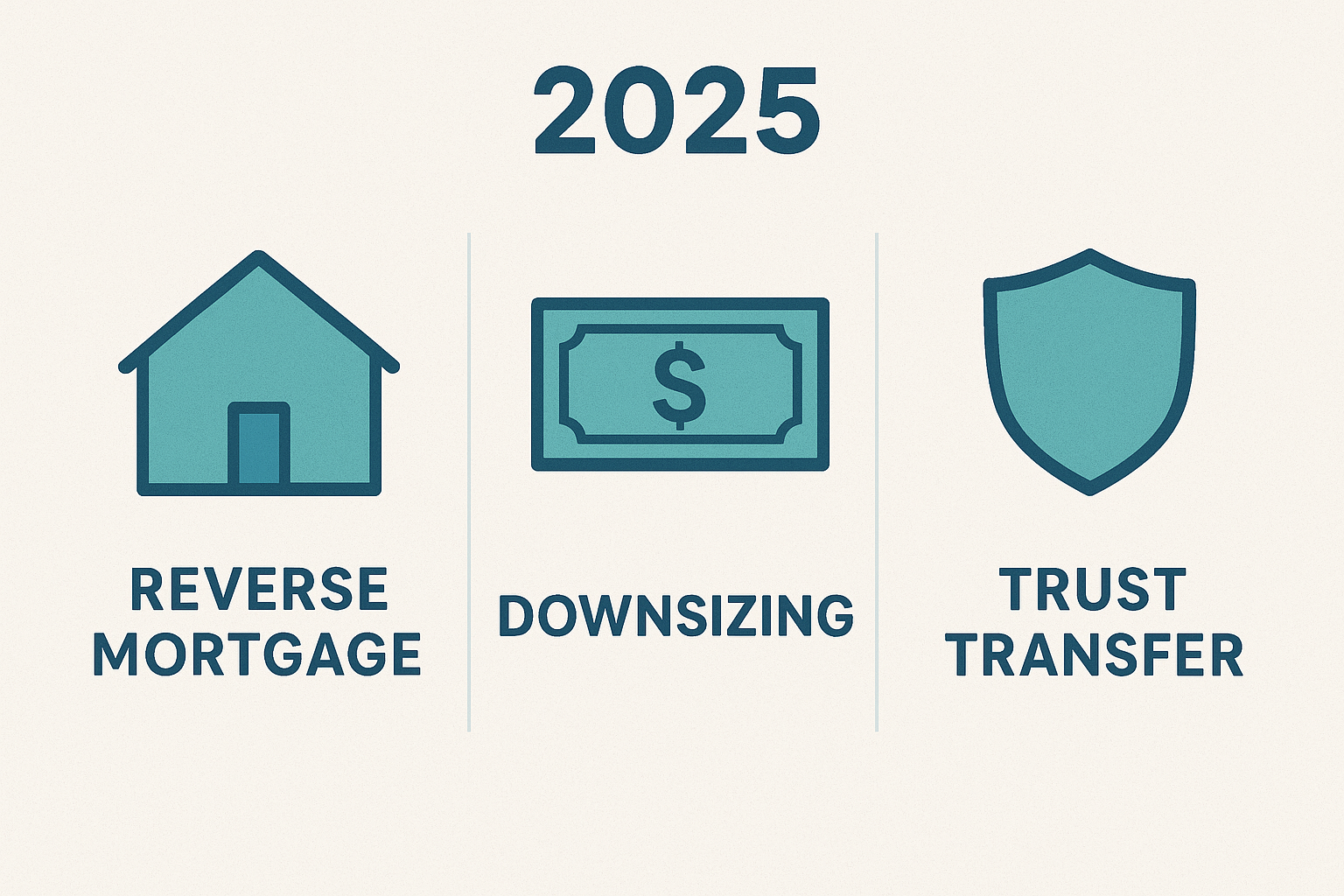

What is a reverse mortgage in 2025? It lets homeowners 62+ borrow against equity, receiving tax-free payments without selling the home.

You keep ownership, and the loan is repaid when the home is sold or upon death.

In 2025, loan limits rise to $1,158,000, reflecting higher home values.

Is it safe? With proper planning, yes—our advisors ensure it fits your goals, avoiding high fees (2–5% of loan value).

How does downsizing help retirement? Selling your home and moving to a smaller, less expensive property frees up equity for income or investments. In 2025, with home prices up 3–5%, this can yield significant cash.

For example, selling a $700,000 home and buying a $400,000 condo nets $300,000. Pairing this with a trust protects proceeds from taxes or Medicaid.

We guide clients through portable trust transfers nationwide.

How do trusts safeguard home equity? Transferring your home to a revocable or irrevocable trust avoids probate (9–18 months, 4–7% costs) and shields equity from Medicaid recovery.

Our cloud-hosted trusts offer free updates, ensuring flexibility across states. This builds on our recent blog, making your plan 2025-ready.

| Option | Benefits | Considerations |

|---|---|---|

| Reverse Mortgage | Tax-free income, stay in home | Fees (2–5%), loan repayment later |

| Downsizing | Large cash influx, lower costs | Emotional ties, moving expenses |

| Trust Transfer | Probate avoidance, Medicaid shield | Requires legal setup, deed filing |

Is a reverse mortgage better than downsizing? It depends—reverse mortgages suit those staying put; downsizing fits those wanting cash now.

Can trusts protect equity from taxes? Yes, especially irrevocable trusts, reducing estate taxes on homes over $13.61 million in 2025. Our 30+ years of expertise ensures clarity.

Unlocking home equity in 2025 can fund your retirement while protecting your legacy. Don’t let 70% of Americans’ planning gaps be your story. Ready to explore your options? Contact Davenport Associates for a free consultation to tailor a plan with reverse mortgages or trusts. You can take our retirement ready quiz to see where you stand as well.