By John F. Davenport, Esq. | Davenport & Associates, Norwalk, CT | May 11, 2026

You spent months working with an attorney to draft a will. Maybe a trust as well. You made decisions about who gets what, named an executor, set up provisions for your children. You felt good about it. The plan was in place.

But there is a form sitting at your brokerage firm, your old employer’s 401(k) administrator, and your life insurance company that you filled out years ago, maybe decades ago, that your attorney has never seen. That form controls what happens to some of your most significant assets when you die. And it does not care what your will says.

A beneficiary designation overrides your will. It overrides your trust. It is, for the assets it covers, the most powerful document in your estate plan. And for most families, those assets are substantial. Americans hold over $9 trillion in IRAs and employer retirement plans alone. Add life insurance, annuities, and payable-on-death bank accounts, and the assets that pass by beneficiary designation easily represent the majority of most families’ wealth.

As both a licensed attorney and a financial advisor, I review beneficiary designations as part of every estate plan review I do. I find problems in the majority of them. Not because people are careless, but because life changes and forms do not update themselves. This post explains exactly how beneficiary designations work, the most common mistakes families make, and how to fix them.

A beneficiary designation is a written instruction you give directly to a financial institution, insurance company, or retirement plan administrator telling them who receives the asset when you die. The asset passes directly to the named beneficiary without going through your estate, without probate, and without regard to your will or trust.

Assets that commonly pass by beneficiary designation include retirement accounts (traditional IRAs, Roth IRAs, 401(k)s, 403(b)s, SEP-IRAs, SIMPLE IRAs), life insurance policies, annuities, payable-on-death (POD) bank accounts, and transfer-on-death (TOD) brokerage accounts.

For most families, these are not minor assets. They are the largest assets they own. And yet many families have not reviewed the forms in years.

| Why the Will Does Not Control These Assets Your will provides instructions for your “probate estate,” which consists of assets held in your individual name without a designated beneficiary. Assets with beneficiary designations, joint ownership with rights of survivorship, or trust ownership all pass outside of probate and outside the reach of your will. If your will says “divide everything equally among my three children” but your IRA form names only your oldest child, the oldest child receives the entire IRA. The will cannot override it. |

This is the scenario that ends up in the news and in court. You got divorced, updated your will, changed your other accounts, but forgot to update the beneficiary designation on a life insurance policy you bought through your employer years ago. You remarried. You have a new family. You die.

Your ex-spouse gets the life insurance proceeds. Your current spouse and children get nothing from that policy. The will, the divorce decree, and your obvious intent are all irrelevant. The form controls.

This happens far more often than people realize. It happens because beneficiary designation forms are completed during busy periods of life (starting a new job, opening an account) and then set aside. Unless someone specifically prompts a review, they sit untouched for decades.

Note: in some states, divorce automatically revokes a beneficiary designation to a former spouse. Connecticut and New York both have statutes that may revoke such designations automatically, but the law is complex, varies by account type, and is not universally applied by all financial institutions. You should not rely on automatic revocation. You should update the form.

Most beneficiary designation forms ask for a primary beneficiary and a contingent beneficiary. The primary beneficiary receives the asset. The contingent beneficiary receives it only if the primary predeceases you. Many people name a primary and leave the contingent blank.

If your primary beneficiary dies before you do and you have no contingent named, the asset typically passes to your estate and goes through probate, which defeats the entire purpose of having a beneficiary designation in the first place. It also opens the asset to creditor claims and can trigger a required distribution within one year at ordinary income tax rates for retirement accounts.

Always name a contingent beneficiary. And if you have multiple contingent beneficiaries, specify the percentage each should receive.

Naming a minor child (under 18 in most states) as a direct beneficiary of a life insurance policy or retirement account creates an immediate legal problem. Financial institutions cannot pay benefits directly to a minor. The money must be held until a court appoints a guardian or conservator to manage it on the child’s behalf.

That process requires a court proceeding, legal fees, bonding requirements for the conservator, annual reporting to the court, and court approval for significant expenditures. It is expensive, slow, and public. It is the opposite of what most parents intend.

The better approach is to name a trust as the beneficiary for a minor’s share and have the trustee manage the funds according to the trust’s terms. An estate planning attorney can draft the appropriate trust language and coordinate it with the beneficiary designation.

Naming your estate as the beneficiary of a retirement account or life insurance policy is almost never the right choice. When the estate is the beneficiary, the asset loses its ability to bypass probate and must go through the court process. It becomes subject to creditor claims. And for retirement accounts, it dramatically accelerates the required distribution schedule.

A non-spouse beneficiary who inherits an IRA has up to 10 years to take distributions under the SECURE Act rules. But if the estate is the beneficiary and the IRA owner had reached their required beginning date, the distributions must typically be taken within five years or on a single lump sum basis, whichever the plan document requires. That can mean a massive taxable income event for the estate.

A common scenario: a couple works with an attorney to create a revocable living trust. The attorney drafts beautifully coordinated provisions for how assets should be distributed. Then the couple goes home and never changes the beneficiary designations on their IRAs, 401(k)s, and life insurance policies from their individual children to the trust.

Result: the trust receives nothing. The assets pass directly and outright to the named beneficiaries, bypassing the trust’s protective provisions entirely. If the trust was designed to include a spendthrift provision, manage funds for a child with special needs, or provide for distributions over time rather than in a lump sum, those protections are gone.

Retirement account beneficiary rules were significantly changed by the SECURE Act (2019) and updated further by SECURE 2.0 (2022). These rules affect how beneficiaries must take distributions and are a critical part of beneficiary planning.

A surviving spouse who inherits an IRA has more options than any other beneficiary. They can roll the inherited IRA into their own IRA and treat it as their own, which means no RMDs until they reach age 73. They can remain as a beneficiary of the inherited IRA and take distributions based on their own life expectancy. This flexibility makes the spouse the most tax-efficient beneficiary for a retirement account.

For most non-spouse beneficiaries who inherit an IRA from someone who died after 2019, the SECURE Act created the 10-year rule. The entire balance of the inherited IRA must be withdrawn by December 31 of the tenth year following the year of death. There is no minimum annual distribution requirement within those 10 years, just a hard deadline at the end.

If the original owner had already reached their required beginning date (age 73) when they died, the beneficiary must also take annual distributions during the 10-year period based on the longer of their own life expectancy or the owner’s remaining expectancy.

The 10-year rule does not apply to eligible designated beneficiaries (EDBs), who can still stretch distributions over their own life expectancy. EDBs include surviving spouses, minor children of the original owner (until they reach majority, then the 10-year rule kicks in), disabled or chronically ill individuals, and beneficiaries who are not more than 10 years younger than the original IRA owner.

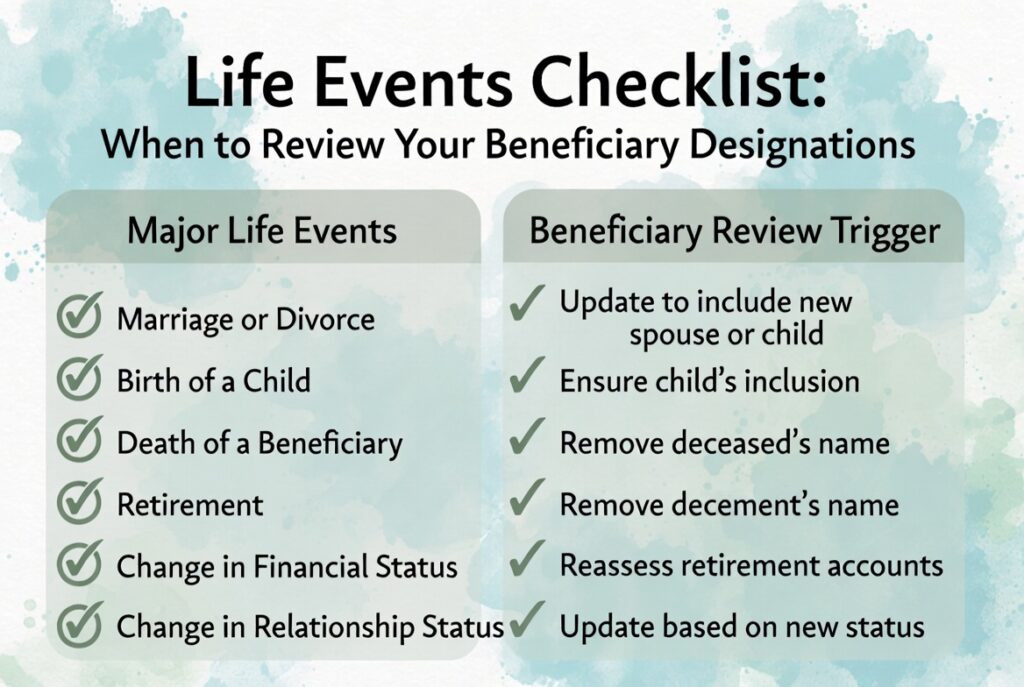

Your beneficiary designations should be reviewed at every major life event. Not just when you create your estate plan, but every time your family circumstances change.

Review them when you get married. When you get divorced. When a child is born or adopted. When a named beneficiary dies. When you remarry. When a child or grandchild reaches adulthood. When you open a new financial account or insurance policy. When you change jobs and roll over a 401(k). When the law changes significantly (as it did in 2019 and 2022 and 2026). And at minimum, every three to five years as a routine review.

Most estate planning attorneys recommend reviewing beneficiary designations annually, as part of a broader financial check-up. The review takes less than an hour and can prevent a disaster that cannot be undone after you are gone.

Start by making a complete list of every account with a beneficiary designation: all IRAs, 401(k)s, 403(b)s, life insurance policies, annuities, POD bank accounts, and TOD brokerage accounts. For each account, contact the institution and request a copy of the current beneficiary designation form on file. Do not assume you know what it says.

Once you have the forms, review each one against your current family situation and estate planning goals. Are the named beneficiaries still the right people? Are the percentages correct? Is there a contingent beneficiary? Is any beneficiary a minor? Does the designation coordinate with your trust?

Then review each account in the context of the broader estate plan. Does the beneficiary designation support or contradict what the will and trust are trying to accomplish? Do different accounts need different beneficiary structures?

Finally, make any needed updates. Contact each institution directly. Do not assume that a change in one account automatically updates others. Each account has its own form and its own process.

These are the questions I hear most from families reviewing their estate plans.

| Q: Does a will override a beneficiary designation? No. A beneficiary designation on an IRA, 401(k), life insurance policy, or annuity overrides your will for that specific asset. The asset passes directly to the named beneficiary regardless of what the will says. Your will only controls assets in your probate estate, which excludes all assets with a valid beneficiary designation. |

| Q: What happens if I have no beneficiary named? The asset typically passes to your estate and goes through probate. For retirement accounts, this can dramatically compress the required distribution period and create a large taxable income event. For life insurance, it means a potentially lengthy court process before your family receives the proceeds. Always name both a primary and a contingent beneficiary. |

| Q: Can I name my trust as the beneficiary of my IRA? Yes, but it must be done carefully. A trust can be a valid IRA beneficiary, but the trust must meet specific IRS requirements to qualify for stretch distribution rules. If the trust does not qualify, the entire IRA may have to be distributed within five years. Work with both an estate planning attorney and a financial advisor to coordinate this properly. |

| Q: What is the 10-year rule for inherited IRAs? Under the SECURE Act, most non-spouse beneficiaries who inherit an IRA from someone who died after 2019 must withdraw the entire balance by December 31 of the tenth year after the year of death. This rule does not apply to surviving spouses, minor children of the original owner (until majority), disabled beneficiaries, chronically ill beneficiaries, or beneficiaries within 10 years of the original owner’s age. |

| Q: Does divorce automatically remove my ex-spouse as beneficiary? Connecticut and New York have statutes that may automatically revoke a beneficiary designation to a former spouse on certain types of accounts after divorce. But the law is complex, inconsistently applied by financial institutions, and does not apply to all account types. You should never rely on automatic revocation. Update the form immediately after any divorce. |

| Q: How often should I review my beneficiary designations? At every major life event (marriage, divorce, birth, death, job change) and at minimum every three to five years as a routine review. Many estate planning attorneys recommend an annual review as part of a broader financial check-up. The review takes less than an hour and can prevent problems that are impossible to fix after you are gone. |

A beneficiary designation form is not a formality. For most families, it controls the distribution of more assets than the will does. And it is the one document in your estate plan that your attorney almost certainly has not seen.

The mistakes that come from outdated or poorly structured designations are not fixable after the fact. An ex-spouse who receives life insurance proceeds because a form was never updated cannot be undone by a court, regardless of intent. A minor child who triggers a conservatorship because they were named directly cannot bypass the process. An estate named as beneficiary cannot retroactively get the stretch distribution rules.

The fix is straightforward while you are alive. Review every account with a beneficiary designation. Update anything that does not reflect your current family, your current estate plan, and your current goals. Make sure everything works together.

If your estate plan was done without a concurrent review of your beneficiary designations, or if it has been more than three years since your last review, you have an incomplete estate plan. That is worth fixing today.

| References & Sources Phillips Lytle LLP: OBBBA 2025, SECURE Act Updates, and Beneficiary Designations in Estate Plans (phillipslytle.com) London Baker Law: Outdated Beneficiary Designations Can Undermine Even the Best Estate Plan, March 2026 (londonbakerlaw.com) IRS: Retirement Topics, Beneficiary (irs.gov) Catalyst Law: Beneficiary Designations Could Override Your Estate Plan, January 2026 (catalystlawllc.com) Hoopes Adams & Scharber: Beneficiary Designations Supersede Wills and Trusts (halaw.com) Edelman Financial Engines: Beneficiary Designation vs Will (edelmanfinancialengines.com) |

| About the Author | John F. Davenport, Esq. John F. Davenport holds a law degree from Pace University, an MBA in finance from Fordham University and undergraduate degree from the University of Notre Dame. He founded Davenport & Associates in 1997 and has spent more than 30 years helping CT and NY locally and families across the country build retirement and estate strategies that work together, not against each other. Davenport & Associates is located at 800 Connecticut Avenue, Suite E401, Norwalk, CT 06854. Phone: (203) 853-6300 | jdavenportassociates.com IMPORTANT DISCLAIMER: Educational only—not investment/tax/legal advice. John F. Davenport is a licensed tax and estate planning attorney. He is not acting as an investment adviser in connection with this content. No strategy guarantees results—vary by rates, markets, laws, personal circumstances. Consult advisors. |